Understanding the Loan Process for Buying a House: Your Essential Roadmap

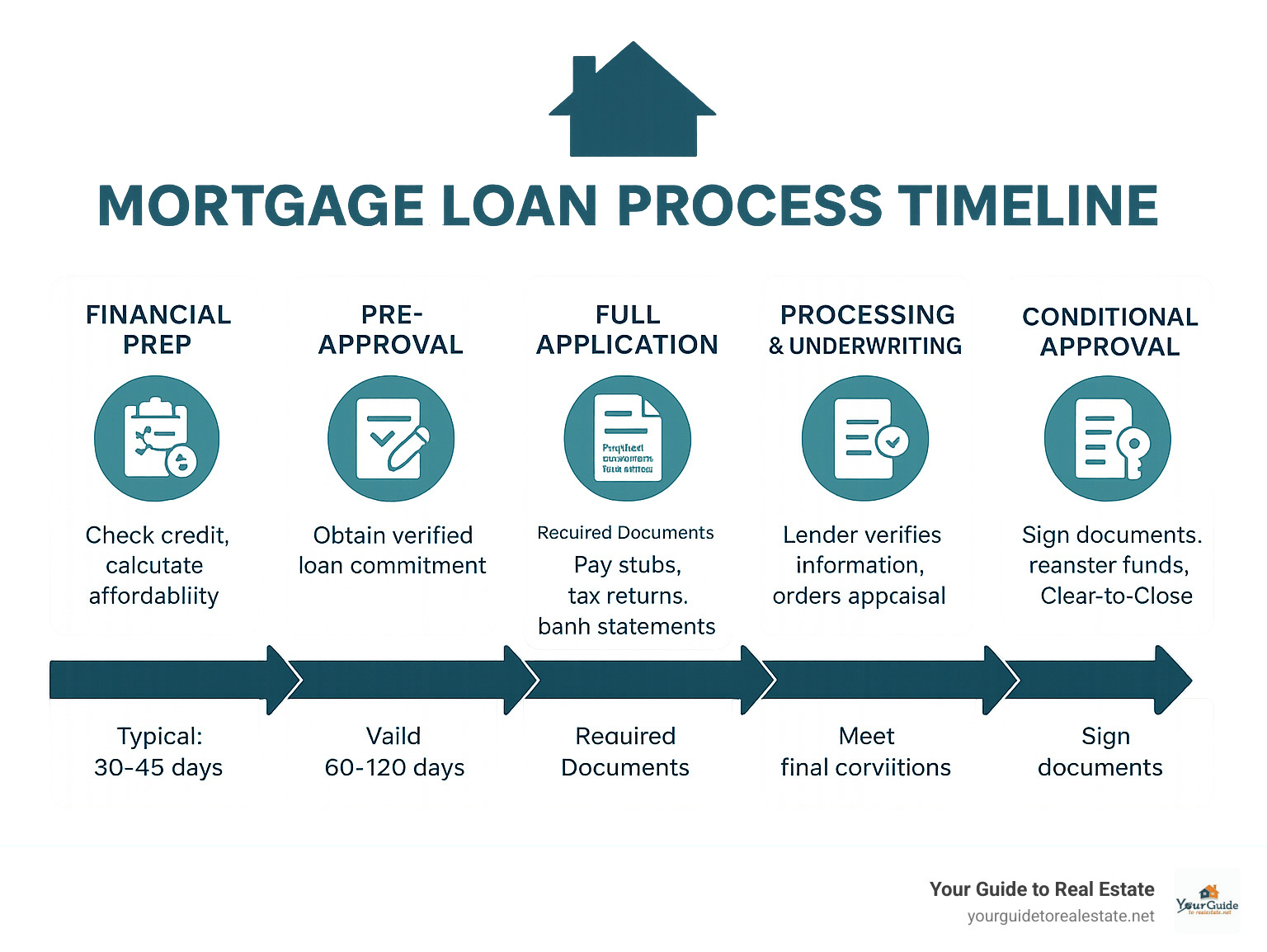

The loan process for buying a house involves six main steps that typically take 30-45 days to complete. Here’s what you need to know:

The 6 Core Steps:

1. Financial prep – Check credit, calculate affordability (39% housing costs, 44% total debt)

2. Pre-approval – Get verified loan commitment from lender (valid 60-120 days)

3. Full application – Submit complete documentation and receive Loan Estimate

4. Processing & underwriting – Lender verifies everything, orders appraisal

5. Conditional approval – Final conditions met, receive Clear-to-Close

6. Closing – Sign documents, transfer funds, get keys

Most people go through these stages when looking for a mortgage: pre-approval, house shopping, mortgage application, loan processing, underwriting, and closing. The process can feel overwhelming, especially for first-time buyers.

But here’s the good news: the mortgage process is relatively simple when broken into clear steps. Getting pre-approved before house hunting strengthens your offers. Closing costs typically run 2-5% of your home’s purchase price. And honest communication with your lender prevents delays.

Handy loan process for buying a house terms:

– easy steps to buying your first home

– fha loan requirements

Why This Guide Matters

We’ve seen too many buyers stumble through the mortgage process without understanding what’s happening or why. This creates unnecessary stress and can even derail your home purchase. When you understand the basics of affordability calculations, lender expectations, and timeline milestones, you’ll approach the process with confidence rather than confusion.

Step 1: Prep Your Finances & Credit

Think of this step as building the foundation for your dream home—except instead of concrete and steel, you’re working with credit scores and bank statements. Getting your finances ready isn’t the most exciting part of the loan process for buying a house, but it’s absolutely crucial.

Your credit score is like your financial report card that lenders use to decide how risky you are to lend to. Most conventional loans require at least a 620 credit score, though some government programs are more forgiving. Your debt-to-income (DTI) ratio is equally important—it shows lenders how much of your monthly income already goes to debt payments. Generally, they want to see your total monthly debts stay under 43-44% of your gross monthly income.

If you’re in Canada, there’s an extra hurdle called the mortgage stress test. This requires you to qualify at either 5.25% or your negotiated rate plus 2% (whichever is higher). The Mortgage Qualifier Tool can help you see exactly where you stand.

Polish Your Credit Profile

Payment history makes up 35% of your credit score, while credit utilization accounts for another 30%. This means you can potentially boost your score fairly quickly by paying down credit card balances and making sure every single bill gets paid on time.

Start by pulling your credit reports from all three major bureaus. You can get these free once a year from AnnualCreditReport.com (the only official site authorized by federal law). Look for anything that seems off—accounts that don’t belong to you, incorrect payment histories, wrong balances, or old negative information that should have fallen off.

Found something fishy? Dispute those errors immediately. Credit bureaus have 30 days to investigate, and fixing mistakes can give your score a nice bump.

Decide How Much House You Can Afford

Here’s where many buyers get themselves into trouble: they focus on the biggest loan amount they can qualify for instead of what they can comfortably afford month after month.

The standard affordability guidelines use two key ratios. Your Gross Debt Service (GDS) should stay under 39% of your household income—this covers your mortgage payment, property taxes, heating costs, and half of any condo fees. Your Total Debt Service (TDS) should stay under 44% and includes all your other debts like credit cards and car loans.

Our Mortgage Payment Calculator Online can help you see how different purchase prices translate to monthly payments. Just because a lender says you qualify for a certain amount doesn’t mean you should borrow every penny.

Step 2: Mortgage Pre-Qualification vs Pre-Approval

Here’s where many buyers get confused in the loan process for buying a house. They think pre-qualification and pre-approval are the same thing—but they’re actually worlds apart. Understanding this difference could mean the difference between your dream home and watching someone else get the keys.

Pre-Qualification: Quick Snapshot

Pre-qualification is your starting point—a casual conversation where you share your income, debts, and savings with a lender. They crunch some basic numbers and give you a rough estimate of what you might be able to borrow. The whole process takes about 15 minutes, and they’ll only do a soft credit pull that won’t ding your credit score.

The catch? Pre-qualification is based entirely on what you tell them. No verification, no document review, no deep dive into your finances.

Pre-Approval: The Real Deal

Pre-approval is where things get serious. Your lender becomes a financial detective, pulling your tri-merge credit report from all three credit bureaus and digging into your bank statements, pay stubs, and tax returns. They’re doing what’s called “underwriting lite”—basically putting your application through the same process you’ll face later, just in advance.

This thorough asset verification process takes several days, but the payoff is huge. You’ll get a commitment letter stating exactly how much the lender will loan you, at what interest rate, and under what conditions. Most pre-approval letters are valid for 60 to 120 days.

Many lenders will also offer rate holds during your pre-approval period, protecting you if interest rates climb while you’re house hunting.

Boosting Your Offer in the Loan Process for Buying a House

When you’re ready to make an offer, your pre-approval letter becomes your secret weapon. It shows sellers you’re not just dreaming—you’re ready to buy. In competitive markets, this seller confidence can tip the scales in your favor.

Your offer will typically include earnest money (usually 1-3% of the purchase price) to show you’re serious, along with smart contingencies that protect you if things go sideways. The stronger your pre-approval, the more comfortable you can be with shorter contingency periods or higher earnest money deposits.

Step 3: Full Loan Application, Documentation & Loan Estimate

You’ve found your dream home and had your offer accepted—congratulations! Now it’s time to dive into the full loan process for buying a house with your complete mortgage application.

The heart of this step is completing the Uniform Residential Loan Application (URLA). It’s basically a detailed form asking about your income, employment history, assets, debts, and the property you’re buying. Most lenders now offer user-friendly online portals where you can fill this out at your own pace, which typically takes 30 to 60 minutes if you have your documents organized.

Once your lender receives your complete application, they’re legally required to send you a Loan Estimate within three business days. The What is a Loan Estimate? guide from the Consumer Financial Protection Bureau explains why this three-page document is so important.

Your Loan Estimate is valid for 10 business days, giving you a comparison window to shop around if you want to explore other options.

Document Checklist & Common Pitfalls

For employment and income verification, you’ll need your W-2 forms from the past two years, recent pay stubs (usually from the last 30 days), and an employment verification letter from your HR department. Don’t forget your tax returns for the past two years.

Self-employed borrowers face extra scrutiny. You’ll need business tax returns for two years, current profit and loss statements, business bank statements, and ideally CPA-prepared financial statements.

For assets and savings, gather bank statements for all accounts from the last two to three months. If someone is giving you gift money for your down payment, you’ll need a gift letter explaining that it’s truly a gift, not a loan.

The biggest pitfalls? Incomplete bank statements, unexplained large deposits, missing signatures or dates on documents, and outdated paperwork that expires after 30 to 60 days.

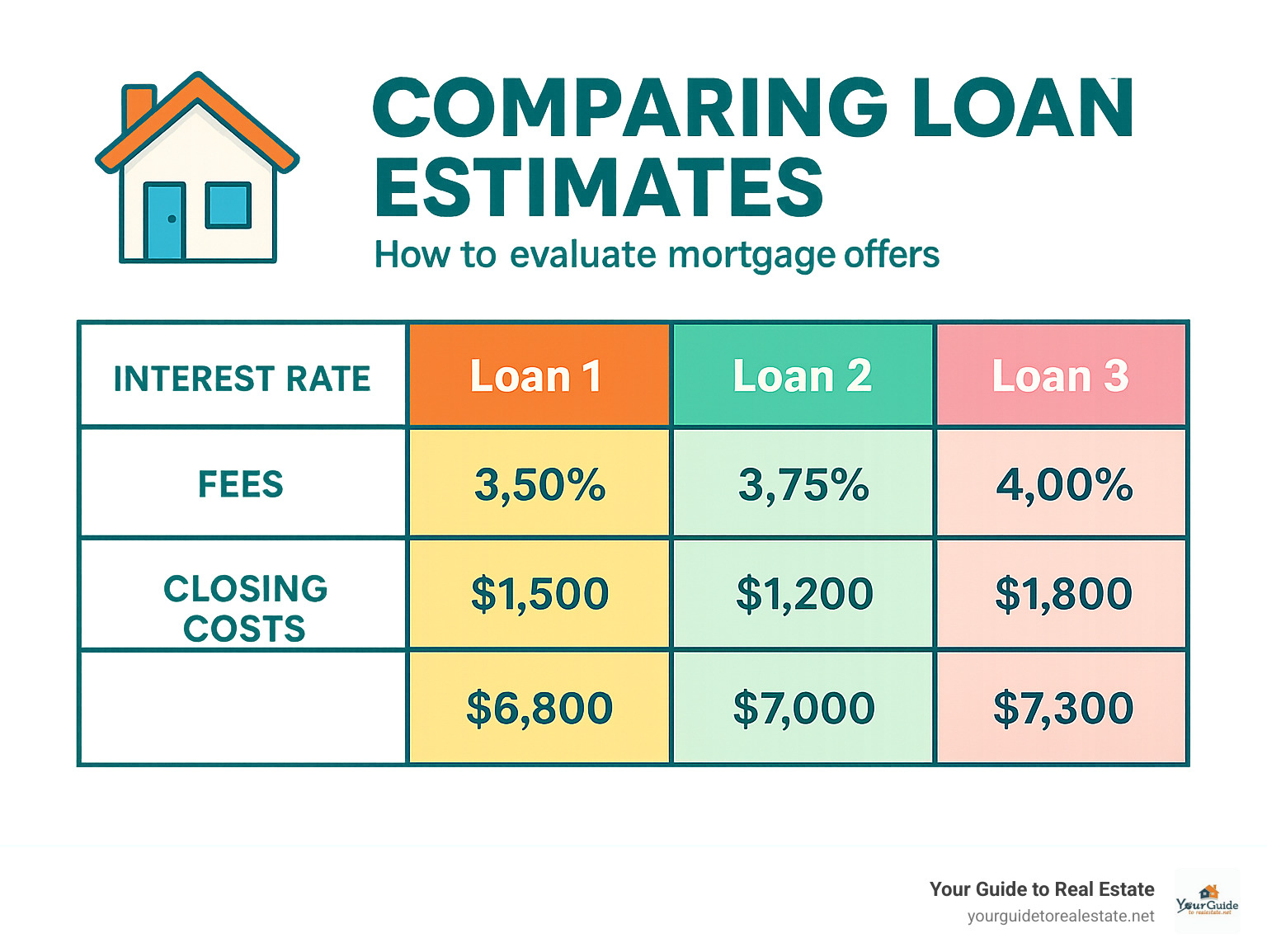

Comparing Lenders Side-by-Side

Shopping around during this stage can still save you thousands of dollars over the life of your mortgage. Our comprehensive guide on How to Compare Mortgages shows you exactly what to look for.

When comparing Loan Estimates, focus on the interest rate and APR first. The APR includes both the interest rate and most fees, giving you a true picture of the loan’s cost. Pay close attention to third-party fees like appraisal costs, title insurance, and attorney fees.

The lowest interest rate isn’t always the best deal. Look at the big picture, including the lender’s reputation for closing loans on time and their customer service quality.

Step 4: From Processing to Underwriting—Inside the Loan Process for Buying a House

Once you’ve submitted your complete application and chosen your lender, your file enters what many consider the most mysterious phase of the loan process for buying a house.

Your loan processor becomes your main contact person during this phase. They’ll order your verification of employment (VOE) and verification of deposits (VOD), arrange the home appraisal, and conduct the title search. If they need additional documents or clarification on something, they’ll reach out to you directly.

Meanwhile, the underwriter is doing the heavy lifting of risk analysis. They’re evaluating what lenders call the “three Cs”: your capacity to repay based on income and job stability, your credit history showing your willingness to pay debts, and the collateral (your future home) that secures the loan.

Appraisal & Home Inspection Essentials

Two important evaluations happen during this stage. The appraisal protects your lender by confirming the home is worth what you’re paying. The home inspection protects you by revealing any safety issues or needed repairs.

Your lender orders the appraisal, which typically costs $400-600 and takes about a week to complete. Licensed appraisers use several valuation methods to determine fair market value.

Here’s what happens if the appraisal comes in low: you can negotiate with the seller to reduce the price, bring extra cash to cover the difference, or request a second appraisal if you believe the first one missed important details.

The home inspection is separate and optional, but we strongly recommend it. For $300-500, a professional inspector examines the property’s structural integrity, electrical systems, plumbing, HVAC, and safety features.

Conditional Approval vs Clear-to-Close: Key Milestones in the Loan Process for Buying a House

Most borrowers receive conditional approval rather than immediate full approval. This simply means your loan looks good, but the underwriter needs a few more items before giving final approval.

Common conditions include explaining recent credit inquiries or large bank deposits, providing updated pay stubs or bank statements, obtaining homeowner’s insurance, or completing minor property repairs.

Clear-to-Close is the milestone you’ve been waiting for. All conditions are satisfied, your loan is fully approved, and you’re ready to sign documents. At this point, your lender will issue the Closing Disclosure, which must be delivered at least three business days before your closing date.

Understanding the Understanding Escrow Process helps you steer these final steps with confidence.

Step 5: Closing Costs, Insurance & Final Walk-Through

You’re almost there! The final step in the loan process for buying a house involves understanding your closing costs, securing insurance, and preparing for the big day when you get your keys.

Closing costs typically run 2% to 5% of your home’s purchase price—on a $300,000 home, that’s $6,000 to $15,000 on top of your down payment. The biggest chunks usually go toward loan origination fees (about 0.5% to 1.5% of your loan amount), title search and insurance ($500 to $1,500), and attorney or notary fees ($500 to $1,000).

Down Payment & Funding Logistics

Your down payment requirements depend entirely on which type of loan you choose. Conventional loans can go as low as 3% down, while FHA loans require 3.5% minimum. If you’re a veteran, VA loans offer 0% down, and USDA loans do the same for eligible rural properties.

But here’s the catch with smaller down payments: if you put down less than 20% on a conventional loan, you’ll pay private mortgage insurance (PMI) every month until you reach 20% equity.

Canadian buyers have different rules. The minimum down payment is 5% for homes up to $500,000. Canadian buyers can tap into their RRSP through the Home Buyers’ Plan (up to $60,000 tax-free) or use the newer First Home Savings Account (FHSA) for tax-free down payment savings.

Your lender will give you specific instructions for bringing money to closing. Usually, this means a certified or cashier’s check for the exact amount, or a wire transfer directly to the title company.

What to Expect on Closing Day

Closing day is when the magic happens—when you officially become a homeowner. The whole process typically takes one to two hours.

You’ll sign the promissory note (your official promise to repay the loan), the deed of trust or mortgage (which secures the loan with your new property), and the closing disclosure that shows the final accounting of all costs.

Make sure you bring your government-issued photo ID, proof of homeowners insurance, certified funds for your down payment and closing costs, and any additional documents your lender requested.

After all the documents are signed and funds change hands, you’ll get those keys you’ve been dreaming about. The deed gets recorded with the local government, making you the official owner.

Frequently Asked Questions: Navigating the Loan Process

How long does the mortgage approval and closing take?

The loan process for buying a house typically takes 30 to 45 days from application to closing. But this timeline can swing dramatically based on your specific situation.

If you’re the ideal borrower with complete documentation ready upfront, a strong credit score above 680, and straightforward W-2 employment, your loan might sail through automated underwriting in just 14 to 21 business days.

Several factors can add weeks to your timeline. Missing or incomplete documentation is the biggest culprit. Self-employment or complex income sources require manual underwriting, which takes longer than automated systems. Credit issues that need explanation can slow things down, as can property problems found during inspection or appraisal.

The key to staying on track? Get your paperwork organized before you even apply, and respond quickly when your lender asks for additional information.

What are common reasons a loan gets denied last-minute?

Credit changes are the number one killer of approved loans. Opening new credit accounts, missing payments, or running up credit card balances can tank your loan even after conditional approval. Your lender will pull your credit again right before closing, so keep your finances frozen until you get those keys.

Employment changes are equally dangerous. Losing your job, switching employers, or moving from salary to commission pay can derail everything.

Financial surprises also cause issues. Large unexplained deposits in your bank account raise red flags. Taking on new debt like a car loan can push your debt-to-income ratio over acceptable limits.

Sometimes the property itself causes problems. If the appraisal comes in significantly below your purchase price, or if major issues are found during inspection, your loan might not go through.

Are there government programs for first-time buyers?

Absolutely! In the United States, FHA loans are incredibly popular because they only require 3.5% down and accept lower credit scores than conventional loans. VA loans offer zero down payment options for eligible veterans and active military members. USDA loans provide zero down payment financing for homes in eligible rural areas.

Canadian first-time buyers have excellent options too. The Home Buyers’ Plan (HBP) lets you withdraw up to $60,000 from your RRSP tax-free for your down payment. The newer First Home Savings Account (FHSA) allows you to save up to $40,000 completely tax-free specifically for your first home purchase.

The key is researching what’s available in your area before you start the loan process for buying a house.

Conclusion

Congratulations! You’ve just walked through the complete loan process for buying a house—from polishing your credit score to holding those shiny new keys. While it might seem like a lot to digest, thousands of people successfully steer this journey every single day.

The secret to a stress-free mortgage experience? Honest communication with your lender and staying organized. Think of your lender as your teammate, not your opponent. They want to close your loan just as much as you want to buy that house.

Here’s what really matters: Get pre-approved before you start house hunting. This single step will save you heartache and strengthen every offer you make. Keep your finances stable throughout the process—no new credit cards, no job changes, and definitely no large purchases on credit.

Budget for closing costs of 2-5% of your home’s purchase price. And please, never be tempted to fudge numbers on your application. Mortgage fraud is a federal crime with serious consequences.

Most importantly, don’t try to go it alone. The loan process for buying a house involves many moving pieces. Work with experienced professionals who can guide you through each step and help you avoid the pitfalls that trip up other buyers.

At YourGuideToRealEstate.net, we’re here to support you throughout your homebuying journey. For even more comprehensive guidance, check out our First-Time Homebuyers Toolkit: Everything You Need to Know Before You Buy.

The path to homeownership might feel long right now, but each step brings you closer to that magical moment when you turn the key in your own front door. With proper preparation, honest communication, and the right guidance, you’ll successfully steer the loan process and secure the financing you need.

Your dream home is waiting—now you know exactly how to make it yours.

")