Why Understanding Mortgage Rates Can Save You Thousands

Understanding mortgage rates is the key to making one of the biggest financial decisions of your life. Whether you’re looking at your first home or trying to decode lender quotes, mortgage rates directly impact how much you’ll pay each month and over the life of your loan.

Here’s what you need to know about mortgage rates:

- Mortgage Rate: The annual interest percentage you pay on your loan balance

- APR: Includes your interest rate plus fees and closing costs for true borrowing cost

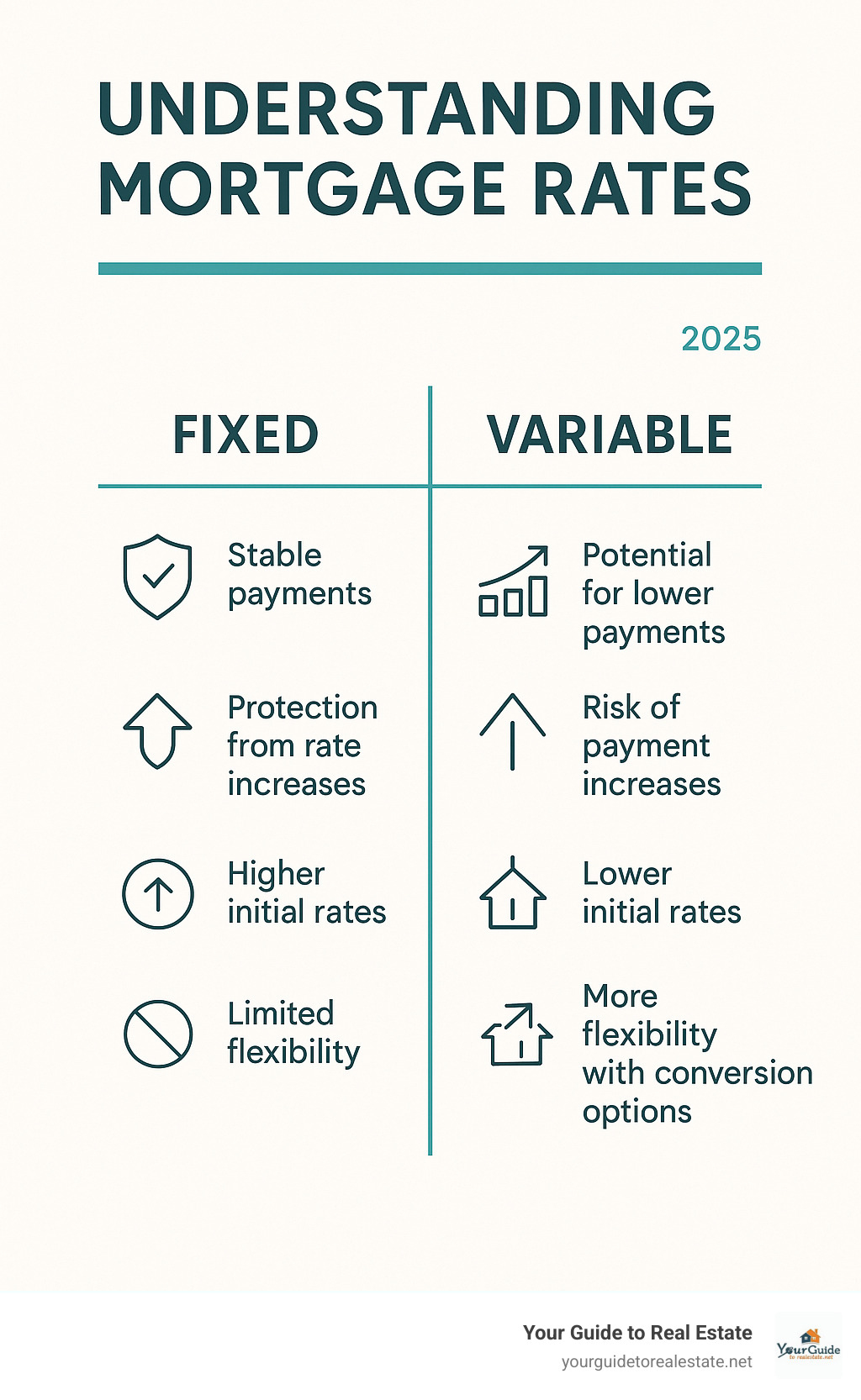

- Fixed Rate: Stays the same for your entire loan term (predictable payments)

- Variable/Adjustable Rate: Can change based on market conditions (lower initial rates but payment risk)

- Rate Factors: Your credit score, down payment, loan type, and economic conditions all influence your rate

The numbers tell a powerful story. Research shows that financing a $436,000 home with 20% down costs $1,749 per month at a 2.6% rate, but jumps to $2,720 monthly at 7.2%. That’s nearly $1,000 more each month – or $11,652 extra per year.

Since 1980, mortgage rates have swung from a high of 18.3% in 1981 to a low of 2.6% in 2020. Today’s rates sit somewhere in between, making it crucial to understand how they work and how to get the best deal possible.

Understanding mortgage rates terms to remember:

– how to shop mortgage

– understanding escrow process

– understanding private mortgage insurance

Understanding Mortgage Rates 101

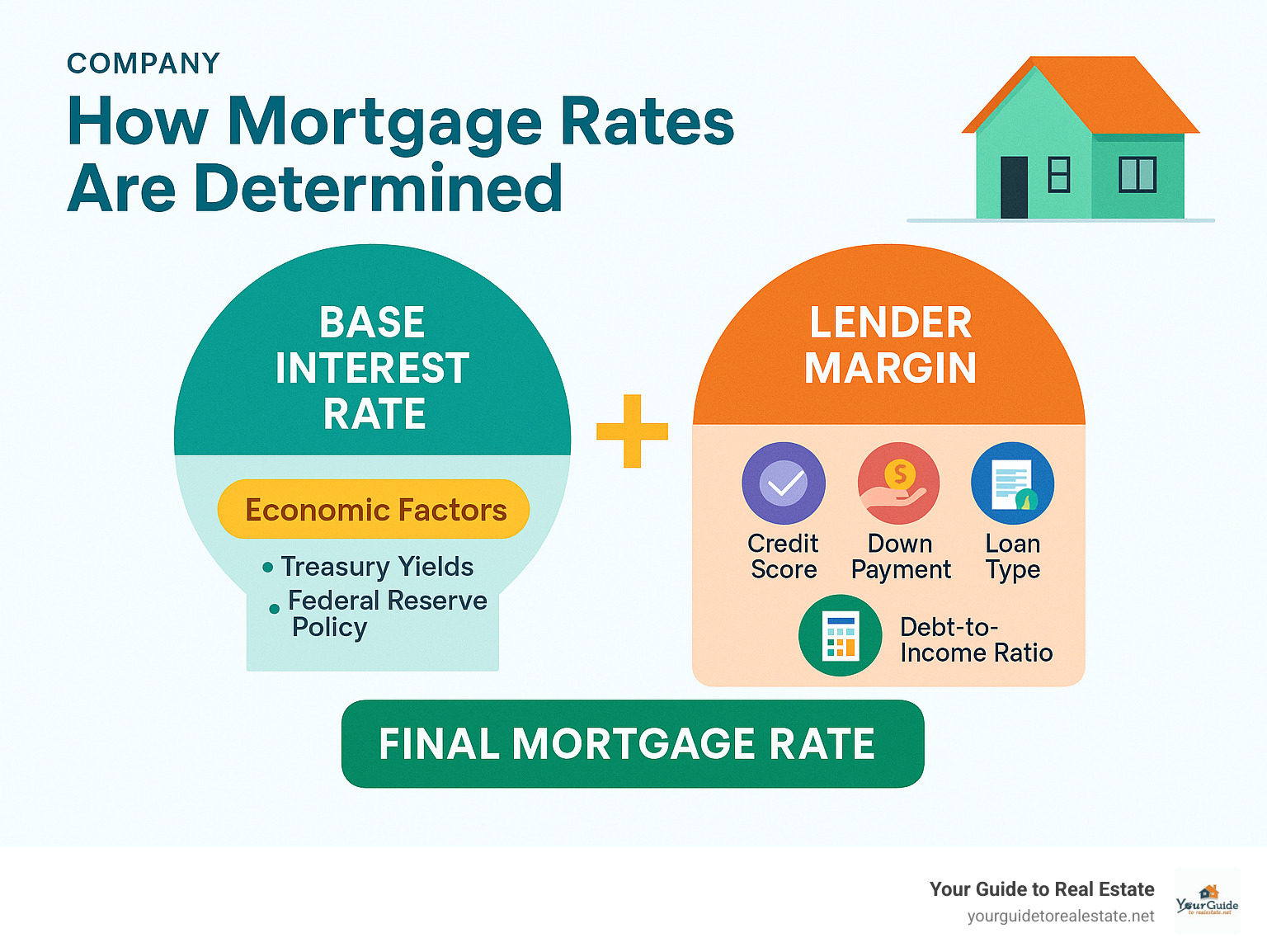

Understanding mortgage rates begins with knowing that your mortgage rate is the annual percentage of interest you’ll pay on your home loan. Think of it as the cost of renting money from a lender.

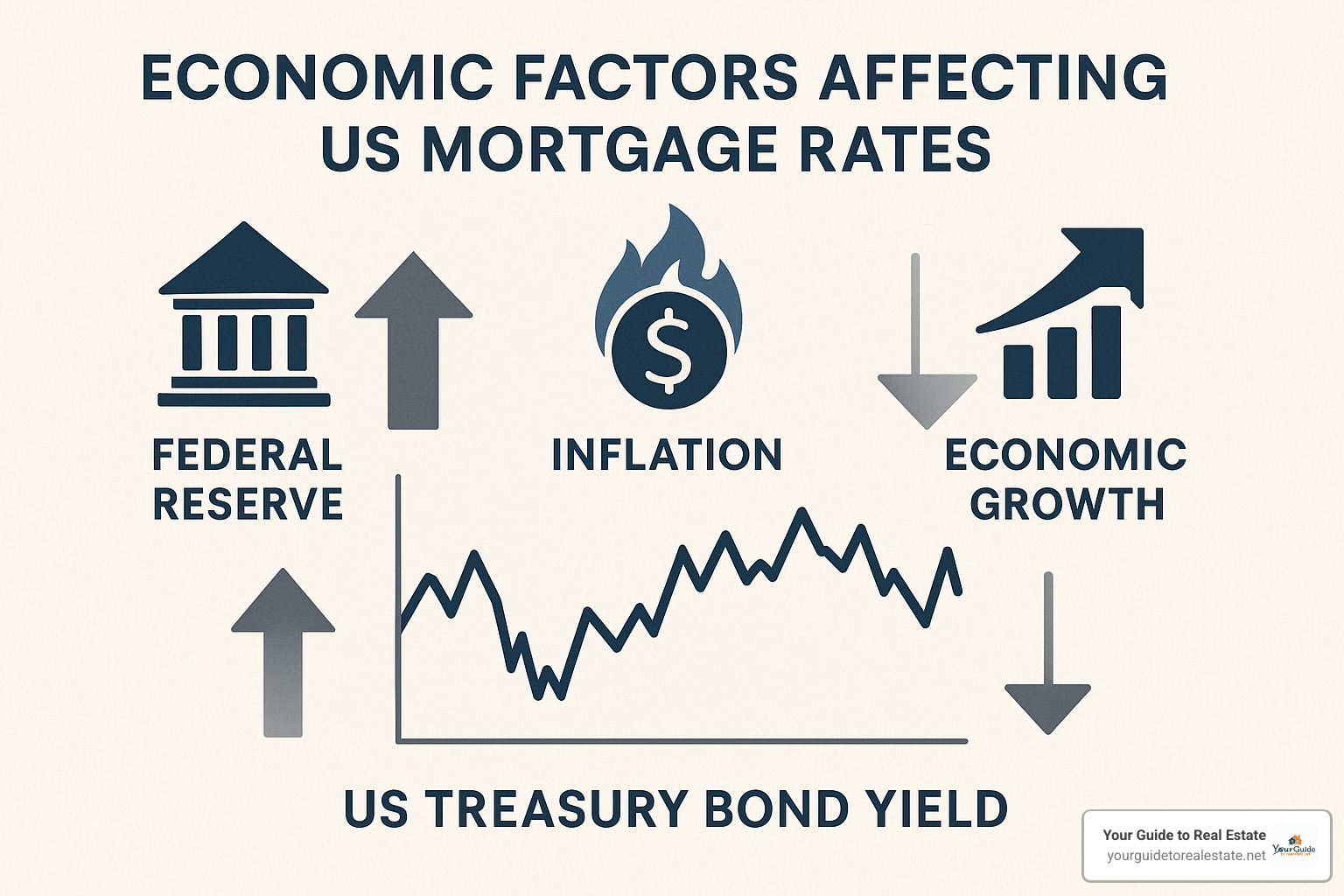

Your rate connects to major financial benchmarks like the 10-year Treasury bond and Federal Reserve policy decisions. When these move, mortgage rates typically follow. Your personal financial picture – credit score, down payment, and debt levels – also plays a huge role in the rate you’ll actually get.

Understanding Mortgage Rates: Definition & Mechanics

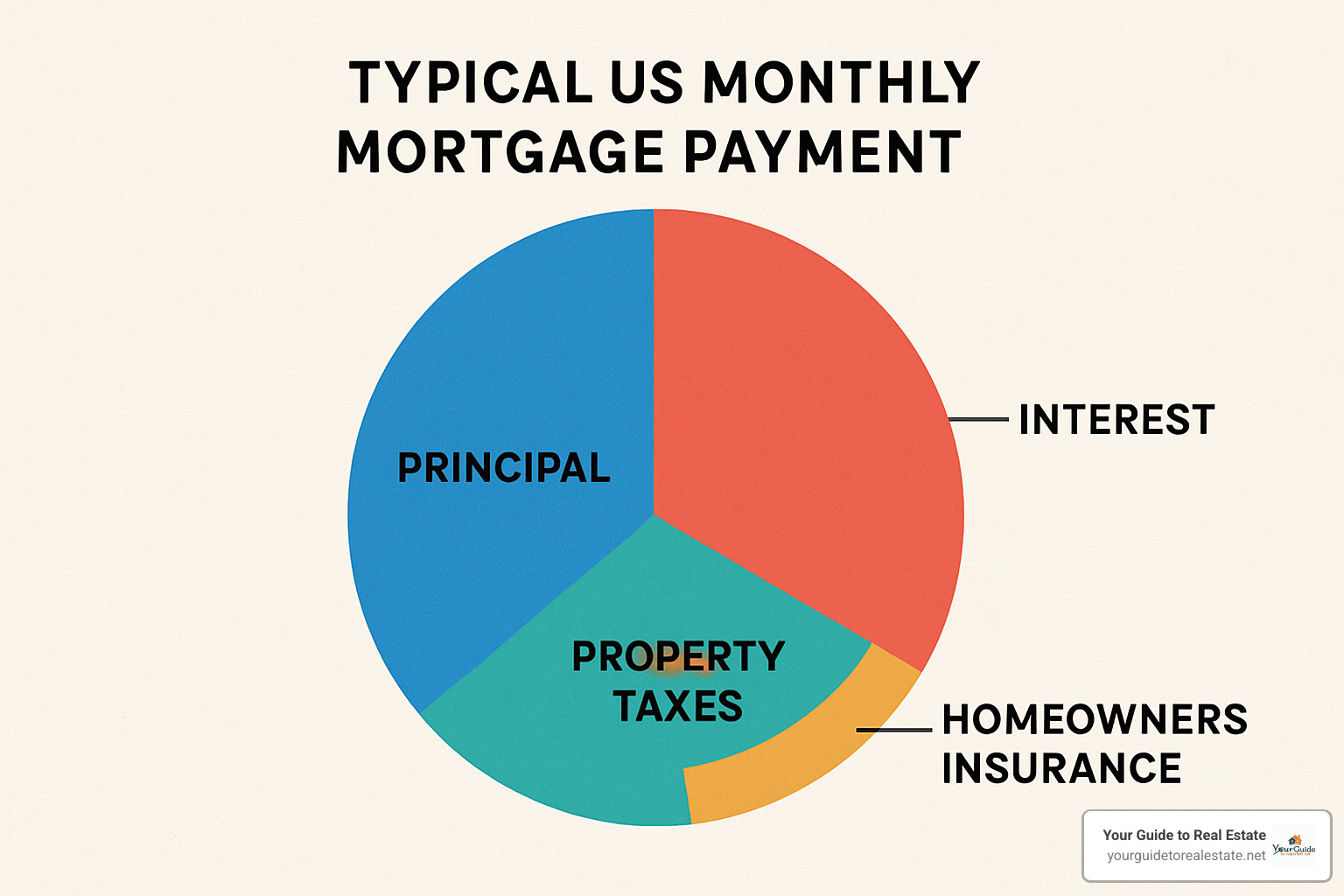

Every month, your payment gets split into two buckets: principal (paying down what you borrowed) and interest (the cost of borrowing). Early in your mortgage, most of your payment goes toward interest. As you chip away at the loan balance over time, more of each payment attacks the principal.

This process is called amortization – gradually paying off your loan through regular payments over 15, 20, or 30 years. The interest compounds monthly on whatever balance remains.

Example: On a $300,000 loan at 7% interest, your monthly payment would be about $1,996. In month one, roughly $1,750 goes to interest and only $246 reduces your loan balance. By year 15, that same payment splits much more evenly between interest and principal.

Understanding Mortgage Rates vs APR

Your mortgage rate tells you the interest percentage, but the Annual Percentage Rate (APR) tells you what you’re really paying to borrow money. The APR includes your interest rate plus origination fees, discount points, broker fees, some closing costs, and sometimes private mortgage insurance.

Example: A lender advertising a 7% interest rate might show a 7.25% APR. That extra 0.25% represents all those fees spread out over your loan term.

When shopping around, focus on comparing APRs rather than just interest rates. A lender with a slightly higher rate but lower fees might actually save you money.

More info about How to Compare Mortgages

Main Mortgage Rate Structures

Fixed-rate mortgages keep your rate exactly the same for your entire term. Your monthly principal and interest payment never changes, making budgeting easy. You’ll typically pay slightly more for this stability.

Variable or adjustable-rate mortgages (ARMs) start with lower rates but can change based on market conditions. In the U.S., these often have a fixed period (5, 7, or 10 years) before adjusting annually. Canadian variable rates tie directly to the lender’s prime rate.

Hybrid mortgages let you split your mortgage – perhaps 60% fixed and 40% variable. This gives partial protection from rate increases while letting you benefit if rates drop.

Closed vs open mortgages: Closed mortgages offer lower rates but limit prepayment options and charge penalties for early payoff. Open mortgages give complete payment flexibility but at higher rates.

Factors That Influence Your Rate

Understanding mortgage rates means recognizing they’re shaped by forces both big and small – from global economic trends you can’t control to personal financial decisions that are entirely in your hands.

Economic Drivers to Watch

Central bank decisions drive the mortgage market more than any other factor. When the Federal Reserve or Bank of Canada raises rates to cool inflation, mortgage rates typically follow within days. These banks meet eight times per year, and their decisions can trigger immediate rate changes.

Bond market performance directly impacts your mortgage rate because most home loans tie to the 10-year Treasury yield. When investors flock to bonds during uncertain times, yields drop and mortgage rates follow. When they sell bonds for stocks, both yields and mortgage rates climb. Mortgage rates usually run about 1.7% above the 10-year Treasury yield.

Inflation and employment data create the backdrop for interest rate decisions. Strong job growth and rising prices signal a hot economy, pushing rates higher. Weak employment and falling prices often lead to lower rates.

Mortgage-backed securities are bundles of home loans sold to investors. Strong demand for these securities pushes mortgage rates down; weak demand pushes rates up.

Latest research on adjustable-rate mortgages

Personal Finance Levers You Control

Your credit score is your most powerful rate-shopping tool. Borrowers with scores of 760 or higher get the lowest advertised rates. Drop to 700-759 and you’ll pay a small premium. Fall to 680-699 and rates become noticeably higher. Below 620 and conventional loans become difficult to qualify for.

Improving your credit score by just 40-60 points can save thousands over your loan’s life.

Down payment size directly affects your loan-to-value ratio. Put down 20% and you eliminate private mortgage insurance while often qualifying for better rates. On a $400,000 loan, the difference between 5% down (7.2% rate) and 20% down (6.8% rate) could save $120 monthly.

Debt-to-income ratio shows lenders how much monthly income goes toward debt payments. They prefer ratios below 36%, though conventional loans allow up to 43%. Lower ratios often qualify for better rates.

Loan type and occupancy create different risk levels. Primary residences get the best rates. Second homes carry premiums of 0.125% to 0.375%, while investment properties face the highest rates – often 0.5% to 0.75% above primary residence rates.

More info about FHA Loan Requirements

Prepayment, Term & Amortization Effects

Loan term length creates interesting trade-offs. Shorter terms like 15 years offer lower interest rates – sometimes 0.5% to 0.75% below 30-year rates. The catch? Monthly payments will be significantly higher.

Amortization periods determine payoff time. In Canada, high-ratio mortgages (less than 20% down) are limited to 25-year amortization. Longer amortization reduces monthly payments but increases total interest paid.

Canadian borrowers face a stress test – you must qualify at the greater of 5.25% or your contract rate plus two percentage points. This ensures you can handle payment increases if rates rise.

Prepayment privileges provide valuable flexibility. Most mortgages allow 10-20% annual prepayments without penalties. Some borrowers choose accelerated biweekly payments, saving tens of thousands in interest over the mortgage’s life.

How to Secure the Best Rate

Getting the best mortgage rate isn’t about luck – it’s about strategy. Research shows that borrowers who don’t shop around typically pay about $300 more per year than those who compare multiple offers.

Tools & Resources for Rate Shopping

The mortgage market is surprisingly competitive. Different lenders have different strengths. Large banks offer convenience, credit unions provide personal service, online lenders have lower overhead, and mortgage brokers work with multiple lenders.

Target at least three different types of lenders to see the full range of available rates. Each evaluates risk differently, meaning the same borrower might qualify for different rates at different institutions.

Pre-approval is your secret weapon for serious rate shopping. Lenders verify your income, assets, and credit to provide rate quotes typically good for 60 to 120 days. This gives you real numbers to compare and shows sellers you’re ready to buy.

Before calling lenders, use mortgage calculators to understand how different rates affect monthly payments and total costs.

Mortgage Affordability Calculator

Use the Mortgage Calculator Tool

More info about How to Shop Mortgage

Paying Points & Larger Down Payments

Mortgage discount points let you buy a lower interest rate by paying extra at closing. Each point costs 1% of your loan amount and typically reduces your rate by about 0.25%.

Example: On a $300,000 loan, one point costs $3,000. If it lowers your rate from 7% to 6.75%, you’ll save about $45 monthly. Your break-even point is 67 months – if you stay longer than 5.6 years, points save money.

The key question is how long you plan to stay. If it’s your forever home, points often make sense. If you might move in a few years, skip them.

Larger down payments continue improving rates beyond 20%. Many lenders offer their best rates at 25% or 30% down, though improvements get smaller as you go higher.

Locking, Floating & Timing the Market

Rate locks protect you from increases but prevent benefiting from decreases. Most lenders offer 30 to 90-day locks, with longer periods available for a fee. Some offer float-down options that protect from increases while capturing decreases.

Timing the mortgage market perfectly is impossible, but watch for signals. Federal Reserve meetings often trigger rate movements. Economic reports like employment data and inflation measures move markets. The 10-year Treasury yield provides a good proxy for mortgage rate direction.

Insider tip: lenders quickly raise rates on bad news but are slower to lower them on good news. When you find a comfortable rate, act decisively rather than waiting for perfection.

Impact on Payments & Overall Affordability

Understanding mortgage rates becomes crystal clear when you see how they translate into real monthly payments and long-term costs. Small rate differences can mean the difference between comfortably affording your dream home and stretching your budget too thin.

Case Study: $436K Home at Different Rates

Let’s examine a $436,000 home with 20% down ($87,200), financing $348,800:

At 2.6% (pandemic low): $1,749 monthly

At 7.2% (recent rates): $2,720 monthly

At 18.2% (1981 peak): $5,695 monthly

That’s almost $1,000 more monthly between low and recent rates – enough for a car payment or vacation fund.

The long-term picture is even more dramatic. Over 30 years, you’d pay $280,640 in total interest at 2.6% rates versus $630,400 at 7.2%. At 1981 rates? You’d pay $1,701,400 in interest alone.

Research shows every 1% increase in mortgage rates reduces buying power by about 10%. If you qualified for a $400,000 home at 5% rates, you might only qualify for $360,000 at 6% rates.

Mortgage Payment Calculator Online

Tax & Insurance Considerations

In the United States, mortgage interest might be deductible if you itemize tax deductions. However, since 2017 tax reforms boosted the standard deduction to $27,700 for married couples filing jointly, fewer people benefit from itemizing.

Many homeowners today don’t get the tax break they’ve heard about. Before factoring mortgage interest deductions into your buying decision, consult a tax professional.

Mortgage insurance affects your bottom line. In Canada, less than 20% down requires mortgage loan insurance for homes under $1 million. Americans face private mortgage insurance (PMI) for conventional loans with less than 20% down, typically running 0.3% to 1.5% of your loan amount annually.

Canadian buyers also face the stress test, requiring qualification at either 5.25% or your actual rate plus two percentage points. This limits borrowing but protects you from getting overextended when rates change.

Renewal, Refinance & Long-Term Strategies

Your mortgage journey doesn’t end at closing. Understanding mortgage rates over the long term means knowing when to make strategic moves that can save thousands.

Most Canadian mortgages get renegotiated every five years, while U.S. borrowers often refinance when market conditions shift dramatically.

Mortgage Renewal Windows

In Canada, lenders must give at least 21 days’ notice before your mortgage term expires. That renewal letter isn’t take-it-or-leave-it – it’s one of your best opportunities to negotiate better terms or shop around.

Don’t automatically sign that renewal offer. Your lender wants to keep your business and will often match competitive rates if you ask. Getting quotes from competitors gives you negotiating power.

When Refinancing Makes Sense

Refinancing means replacing your current mortgage with a new one, hopefully with better terms. Consider refinancing when:

- Rates have dropped significantly – typically 1% to 2% below your current rate

- Your credit score has improved 50+ points since getting your mortgage

- You want to access home equity for renovations or investments

- You want to switch from variable to fixed for payment predictability

Understanding Break Costs

Before refinancing, understand the penalties. Breaking a fixed-rate mortgage early typically involves interest rate differential (IRD) penalties, sometimes tens of thousands of dollars. Variable rate mortgages usually charge just three months’ interest as penalty.

Always calculate break costs against potential savings. Sometimes the penalty math doesn’t work, even if rates have dropped significantly.

Home Equity Credit Lines

A HELOC lets you borrow against home equity at variable rates, usually prime plus 0.5% to 1%. This can be useful for major expenses like renovations, education, or investments. Remember – you’re putting your home on the line, so use this tool wisely.

Cash-Out Refinancing and Term Changes

Sometimes refinancing isn’t about better rates – it’s about accessing equity or changing payment structure. Cash-out refinancing lets you borrow more than you owe and pocket the difference.

You might also want to shorten your term to pay off faster, or extend it to reduce monthly payments during tight financial periods.

More info about Mortgage Refinancing Explained

The key to long-term mortgage success is staying informed about your options and being ready to act when opportunities arise.

Frequently Asked Questions about Understanding Mortgage Rates

How often do mortgage rates change?

Mortgage rates can shift multiple times throughout a single day, like stock prices responding to financial markets. The driving force is the mortgage-backed securities market, where your future loan payments get bundled and traded among investors.

Most lenders update their official rate sheets once or twice daily. During calm periods, rates might hold steady for days or weeks. During volatility – like major Federal Reserve announcements – rates can bounce significantly within hours.

This daily fluctuation is why timing matters when you’re ready to lock in your rate.

Are mortgage interest payments tax-deductible?

In the United States, mortgage interest on your primary residence is deductible – but only if you itemize deductions instead of taking the standard deduction. Since 2017 tax reforms significantly increased standard deduction amounts, fewer people find itemizing worthwhile.

For 2023, the standard deduction is $27,700 for married couples filing jointly and $13,850 for single filers. Your mortgage interest plus other itemized deductions needs to exceed these amounts before you see any tax benefit.

Many homeowners with moderate mortgage balances end up taking the standard deduction anyway, making the mortgage interest deduction irrelevant.

In Canada, mortgage interest on your primary residence generally isn’t tax-deductible, though you can typically deduct interest on investment properties.

What’s the difference between open and closed mortgages?

You’re choosing between flexibility and savings – like a discount airline ticket with restrictions versus a full-price changeable ticket.

Closed mortgages offer the attractive lower rates you see advertised. The trade-off is limited prepayment flexibility. You can usually make extra payments of 10-20% of your original principal annually without penalties, but paying off the entire mortgage early triggers substantial penalty fees.

Open mortgages provide complete freedom to make unlimited prepayments or pay off your mortgage entirely without penalties. The cost? Interest rates running 1-2% higher than closed mortgage rates.

For most homeowners, closed mortgages make financial sense. The rate savings over five years typically outweigh prepayment restrictions. Open mortgages work best when you know you’ll be paying off your mortgage quickly through a planned sale or expected windfall.

Conclusion & Next Steps

Congratulations! You’ve mastered the fundamentals of understanding mortgage rates – knowledge that can save you thousands over your loan’s life. The mortgage world might seem complex, but you now understand the key pieces.

Mortgage rates aren’t random numbers. They’re influenced by Federal Reserve decisions to your personal credit score. The APR gives you real cost comparisons between lenders, while choosing between fixed and variable rates depends on your comfort with payment predictability versus potential savings.

Here’s what matters most: Credit scores above 760 open up the best available rates. A 20% down payment eliminates mortgage insurance and opens better pricing. Shopping multiple lenders saves the average borrower over $300 annually. If you’re staying put for years, discount points might pay for themselves.

Your next steps are straightforward:

- Check your credit score and dispute any errors

- Calculate your affordability at current rates using online tools

- Get pre-approved with at least three different lenders to compare real offers

- Keep an eye on economic indicators like Federal Reserve announcements

- When you find a competitive rate, lock it in rather than trying to time the market perfectly

The mortgage landscape keeps evolving, but these core principles remain your foundation. Whether buying in a low-rate environment or navigating higher rates, informed borrowers always come out ahead.

Small rate improvements compound into serious savings. The difference between 6.5% and 7% rates on a $400,000 loan costs about $120 extra monthly – that’s $43,200 over 30 years. Your effort to understand and optimize your mortgage rate ranks among the most valuable investments you’ll ever make.

As Your Guide to Real Estate, we’re committed to helping you steer these important financial decisions with confidence and clarity.

More info about Understanding Mortgages: A Beginner’s Guide to Home Loans

Ready to put this knowledge into action? Armed with everything you’ve learned here, you can approach lenders from a position of strength and understanding. Your future self will thank you for mastering understanding mortgage rates – it’s knowledge that pays dividends for decades to come.

")